- News

- Pent-up leasing demand for new offices may be unleashed in H2 2024

Pent-up leasing demand for new offices may be unleashed in H2 2024

MOST property consultants are expecting Singapore Central Business District (CBD) Grade A office rents to post another year of modest growth in 2024, amid substantial islandwide completion of nearly 3 million square feet (sq ft) of new office space and cautious business sentiment.

“In the near term, market power may shift away from landlords as more options are at hand for tenants. Vacancy and rents may come under further pressure from the increasing amount of available space,” said June Chua, executive director and head of tenant representation at Colliers.

“In an uncertain environment, tenants are more likely to consider consolidation and renewals than expansion or relocation,” she added.

Cushman & Wakefield’s co-head of commercial leasing for Singapore, Leong Deyang, said: “The cumulative effects of heightened interest rate levels would continue to weigh on overall leasing demand.”

"A lot of leasing decisions being made in 2023 will result in some space returning to the market in 2024." - Andrew Tangye of JLL

On a positive note, however, Leong said that tech demand may surprise on the upside in 2024 in light of positive earnings announcements and a rally in tech stock prices.

Cushman is predicting up to a 2 per cent rise in average rental for its basket of CBD Grade A office space in 2024 following a 3 per cent increase in 2023, a slowdown from the 6.5 per cent growth in 2022. Knight Frank, too, expects rents to grow more moderately between 1 and 3 per cent next year, following a 4.1 per cent rise in 2023. In 2022, rents tracked by Knight Frank went up 5.5 per cent.

CBRE’s head of research for Singapore and South-east Asia, Tricia Song, said that there could be a softening of sentiment in 2024 due to the slew of supply – from the delayed completion of IOI Central Boulevard Towers in the core CBD to projects such as Keppel South Central in the fringe CBD and Labrador Tower and Paya Lebar Green in decentralised locations. In total, 2024 will contribute about 2.9 million sq ft of new supply islandwide, well above the 10-year (2014 to 2023) average of 1.23 million sq ft.

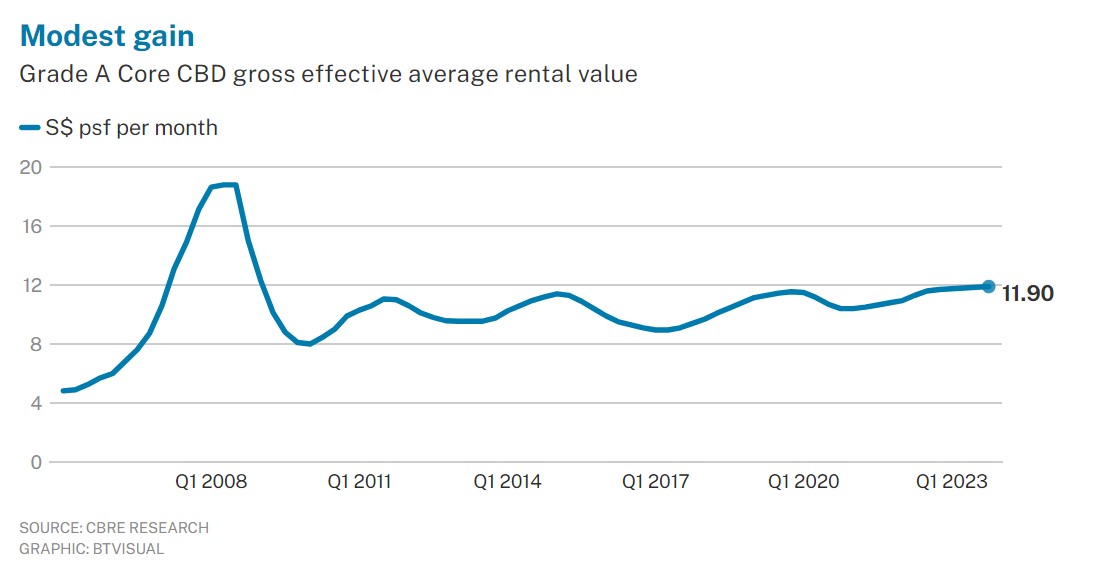

Nevertheless, citing an improvement in the Singapore economy, CBRE expects the gross effective average monthly rental value of its core CBD (Grade A) office basket to climb at a faster clip of 2 to 3 per cent in 2024, outperforming the 1.7 per cent increase this year to S$11.90 per square foot (psf).

2024, a year of two halves

JLL’s head of research and consultancy for Singapore, Tay Huey Ying, predicts a year of two halves. Soft occupier sentiment could continue in the next six months, keeping CBD Grade A office rent muted. “However, pent-up demand could be unleashed by H2 2024, should economic prospects brighten to lift business confidence and spur occupiers to revive expansion plans.”

She added: “This could stimulate office take-up and drive rental growth in the second half, potentially generating full-year rent increase of within 3 per cent.” JLL has estimated the average monthly rental value of its basket of CBD Grade A offices at S$11.27 psf by end-2023, representing a 0.7 per cent year-on-year rise.

Tay forecasts that the average vacancy rate for the same basket will rise from an estimated 5.5 per cent at end-2023 to around 8 per cent at end-2024. “This will stem largely from the substantial completions scheduled for 2024 and the time needed for occupiers to fit out their premises prior to moving in, which in some cases could take place only in 2025.”

"Rewiring of supply chains will lead to some MNCs expanding in neighbouring countries and start basing more staff there permanently." - Alan Cheong of Savills

Savills Singapore’s executive director for research and consultancy Alan Cheong holds a different view, with his forecast that Grade A CBD office rents will slip 2 to 3 per cent next year. For 2023, rents rose by 1.1 per cent. “If we break it down qualitatively, we find that rents in some Grade AAA buildings are rising while others are holding firm. But for AA and A-grade buildings, there is more room for negotiation.”

He cited a string of reasons for predicting a rental drop over the next 12 months. “A high operating-cost base in Singapore, coupled with challenging business conditions, may induce companies to pare their headcounts and office space footprint to save costs.”

“The rewiring of supply chains will lead to some multinationals expanding operations in neighbouring countries, to a point that they start basing more staff there permanently – instead of housing them in Singapore to do regional work,” noted Cheong.

He added that CBD Grade AA and A offices may see higher vacancy rates, with landlords more willing to negotiate on the rent.

However, if the United States manages to avoid recession and interest rates decline sharply, companies can breathe easier and afford to allocate a bigger capital expenditure (capex) budget for new fit-outs. This will incentivise relocations and boost new leasing demand.

Cheong also envisages a bright spot in the next wave of tech demand coming potentially from artificial intelligence set-ups.

"Some shadow spaces were also taken off the market as tech occupiers decided to retain their office premises." - Tricia Song of CBRE

Calvin Yeo, managing director of occupier strategy and solutions at Knight Frank Singapore, said that as businesses tighten hybrid working policies with back-to-office momentum, workplace well-being and the provision of facilities that support physical and mental health have become important in retaining and attracting talent. These include access to gyms and social spaces.

This year, agents noted that a key feature of the Singapore office market has been few large new leasing deals. Said Savills’ Cheong: “For tenants whose leases were due in 2023, most either retained their footprint or contracted by 10 to 20 per cent if they opted for the hybrid-work model. A lack of a capex budget for new fit-outs forced them to remain in the same building.”

David McKellar, co-head of office services, Singapore, at CBRE, highlighted that the vacancy in the core CBD (Grade A) segment remained tight this year due to limited supply, leading some occupiers to renew existing leases at higher reversionary rents rather than relocate, given high capex and interest rates.

Leong of Cushman saw some tenants facing “increased decision paralysis” on their space needs in an uncertain interest rate environment and weakening economic outlook. “As a result, we saw more short-term lease renewals rather than large-scale relocations or expansions, as real-estate decisions are delayed.”

“Landlords typically ask for higher rents for short-term lease renewals, and this had an inflationary effect on rents in 2023.”

Shadow stock shrinks

Office-market observers noted an improvement in the stock of shadow space, which is excess space on an existing lease obligation that a tenant would like to give up by finding a replacement tenant for the landlord. Industry players track this metric for a fuller picture on vacancy.

Cushman estimated that the islandwide shadow office stock has shrunk from 639,000 sq ft as at end-2022 to about 340,000 sq ft as at end-2023.

Andrew Tangye, head of office leasing advisory at JLL, which has similar shadow space numbers, said that the significant reduction has come as many of these spaces have been successfully re-let or taken back by the occupier for self-use. “The quantum of shadow space currently in the market is not significant when compared with, post-GFC (global financial crisis) in 2009, where it peaked at just over 1 million sq ft,” he added.

CBRE data showed that shadow space fell from 460,000 sq ft to 170,000 sq ft. “Occupiers gravitated towards these shadow spaces, as they seized the opportunity to move into high-quality, fitted office spaces in the prime Marina Bay and Raffles Place areas. Some shadow spaces were also taken off the market as tech occupiers decided to retain their office premises,” said Song.

Plum CBD offices given up by tenants seem to be finding takers steadily.

Tangye cited some examples. In 2023, Blackstone moved into the top two floors at Marina Bay Financial Centre Tower 1 that were formerly occupied by Standard Chartered Bank. Also this year, Eastspring Investments leased a floor at Marina One East Tower that was formerly occupied by PwC, while Liberty Insurance took up 18,000 sq ft formerly occupied by Crypto.com at One Raffles Quay North Tower.

According to another leasing agent, at CapitaGreen, Rakuten has leased 44,000 sq ft that was given up by X. JLL is understood to have brokered the deal.

The season of tenants wanting to give up excess space is not likely to end anytime soon. As JLL’s Tangye observed: “When firms embrace hybrid working and move away from assigned seating, it typically decreases the demand for space needed. A lot of leasing decisions being made in 2023 will result in some space returning to the market in 2024.”

More News

GuocoLand taps X factor to help tenants pull workers to offices amid hybrid work

It finds that Grade A office buildings need to have a range of amenities, be in a vibrant location for greater appeal to occupiers seeking to build social capital Read MoreSingapore offices await a new wave of tenants

Landlords don’t know who the next occupants will be as the tech industry cycle which has provided demand for working spaces comes to an end Read MoreSingapore office rents in central region fall 1.7 per cent in Q1 after rising for 9 quarters

Tech, flexible space and traditional banking sectors adopt more conservative stance, mitigating rent-increase pressures Read MoreDBS puts 46 retail units, HDB shops on market for S$210 million

The units, previously occupied by full-service bank branches, are in places such as Bishan, Jurong West and Thomson Plaza Read MoreCiti Commercial Pte Ltd is founded in 2009. Since then, we have created a strong market presence in the commercial real estate consultancy with our dedication and consistent good service.

© Copyright 2024 Citi Commercial Pte Ltd :: Agency Licence No. L3009610D