- News

- Islandwide net office demand nearly doubles in 2023, URA central region office index up 13.1%

Islandwide net office demand nearly doubles in 2023, URA central region office index up 13.1%

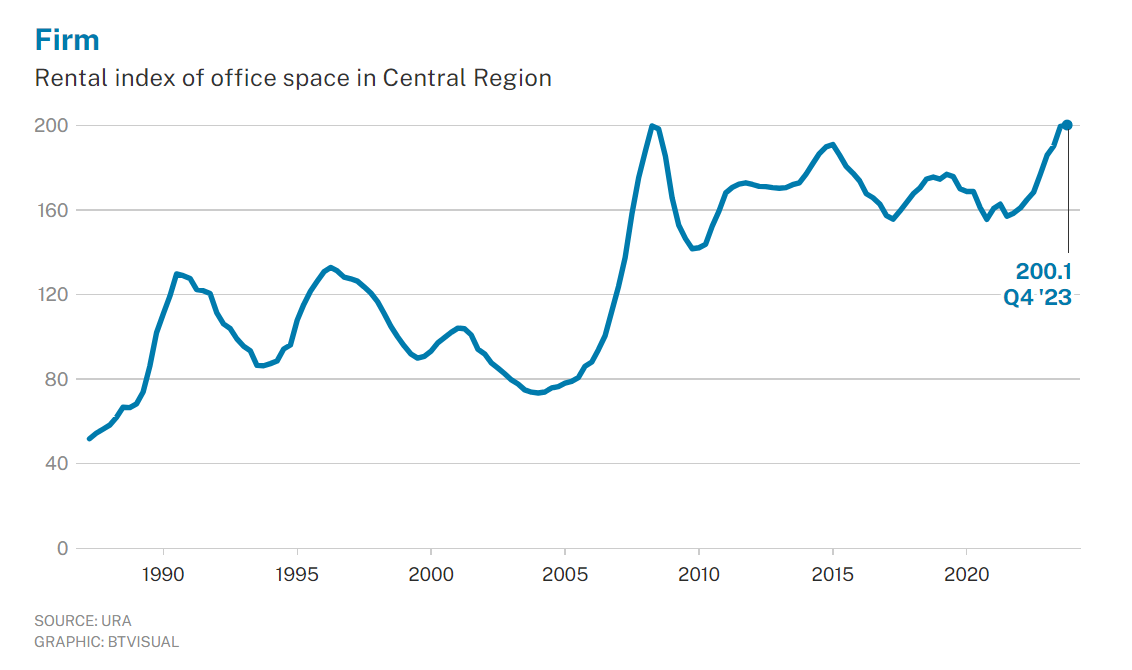

THE Urban Redevelopment Authority’s (URA) office rental index for Singapore’s central region rose 0.3 per cent in the fourth quarter of 2023 over the preceding quarter.

This was a slower increase than the 4.9 per cent gain in Q3 2023. For the whole of 2023, the office rental index climbed 13.1 per cent after expanding 11.7 per cent in 2022.

URA data released on Friday (Jan 26) also showed that the price index of office space in the central region fell 5.9 per cent in Q4 2023 from the previous quarter, contrasting with a quarter-on-quarter increase of 0.8 per cent in Q3 2023. For the whole of 2023, the office price index eased 4.2 per cent after dipping 0.1 per cent in 2022.

The amount of occupied office space increased by about 96,900 square feet (sq ft) in net lettable area (NLA) in Q4 2023, down from the increase of 247,600 sq ft in the previous quarter. The islandwide vacancy rate for office space dipped to 9.9 per cent as at the end of Q4 2023, from 10 per cent as at end of the Q3 2023.

Colliers’ head of research for Singapore Catherine He said: “Although the overall statistics portray a healthy Singapore office market with tight vacancy, it also points to slowing demand and moderating rental growth.”

She noted the widening gap between landlords’ and tenants’ expectations. “Landlords are still expecting higher rents but face increasing resistance from tenants, especially under this weaker economic climate. However, market power may shift away from landlords in the next few quarters as more primary and secondary spaces come to the market, putting further pressure on occupancy and rents,” said He.

Colliers expects the annual growth for URA’s office rental index in the central region to moderate to between 3 per cent and 5 per cent for 2024.

Knight Frank forecasts that the average gross effective monthly rental value for its CBD Grade A office basket will post more moderate growth of 1 to 3 per cent for the whole of this year, after rising 4.1 per cent in 2023 and 5.5 per cent in 2022.

“Most office occupiers are likely to remain cautious in expanding; 2024 has begun with headlines of retrenchment news, especially in the technology sector. The slight growth in rents projected for 2024, notwithstanding the infusion of supply, is due to most buildings in this segment currently enjoying tight occupancies,” said the property consulting group’s head of Singapore research, Leonard Tay.

The 13.1 per cent full-year increase in URA’s central region office rent index in 2023 (most of which was in the first three quarters) was much higher than the rental gains reflected for CBD Grade A office baskets of most property consultancies.

Different computation

Alan Cheong, executive director at Savills Singapore, said one possible explanation for the variance may be that the URA office rental indices are computed based on the lease commencement date. Meanwhile, property consultants could be recording the rents at the point where the lease was contracted, which would be earlier. “For 2022 to early 2023, the chatter of layoffs in the tech sector was not as loud as what was heard in H2 2023. What this could mean is that in 2024, the URA office rental index may start to stabilise or even decline slightly as leases contracted in 2024 mature to commencement in 2025,” he added.

This year, Savills is forecasting a rental drop of 2 to 3 per cent for its basket of Grade A CBD office rents; last year, rents went up 1.1 per cent, after increasing 2.2 per cent in 2022. Cheong cites, among other factors, a high operating cost base in Singapore. Coupled with challenging business conditions, that may induce companies to pare headcounts and office space footprint to save costs.

URA data shows that islandwide net new office demand, as measured by the change in occupied office space, nearly doubled to about 893,400 sq ft in 2023 from 473,600 sq ft in 2022, bolstered by strong demand from the Downtown Core (which includes locations such as Raffles Place, Marina Bay and Shenton Way).

In tandem with this, noted analysts, URA’s median monthly rental (based on contract date) for Category 1 offices (covering the better-quality buildings in the city area) rose 7.2 per cent for the whole of 2023 to S$11.52 per square foot (psf), surpassing the 6 per cent rent increase for Category 2 (which covers the remaining office space in Singapore) to S$6.04 psf. The vacancy rate for Category 1 offices has fallen to 7.5 per cent as at end-2023 from 9.5 per cent at end-2022.

Flight to quality persists

Wong Xian Yang, head of research for Singapore and South-east Asia at Cushman & Wakefield, said: “A flight to quality continues to sustain as occupiers look for better quality and located office space, though they may take up a smaller footprint as they adopt hybrid work arrangements.”

He added that this year, office rents in the central region could continue to slow as supply and demand rebalance against the backdrop of still-high interest rates and more supply. IOI Central Boulevard Towers, Labrador Tower and Paya Lebar Green, which are all expected to complete in 2024, will contribute about 2.3 million sq ft of new office stock, on top of a potential build-up of secondary spaces (that is, space vacated in existing buildings). That said, he noted that about 43 per cent of this new supply has been pre-committed as at end-2023.

Another potential positive is that office relocation and expansion activities in the central region could pick up in the second half of 2024, with more options in the market and a potential easing of capital expenditure constraints with better economic conditions. “In particular, the pent-up demand for office spaces could be building up. As many occupiers have kept their office footprints unchanged or right-sized since the pandemic, some offices are becoming more crowded amid rising office-using employment and a widespread push for return-to-office policies,” said Wong.

The substantial quarter-on-quarter drop in URA’s price index for office space in Q4 2023 left some observers scratching their heads. Offering an explanation, Wong of Cushman said: “It could be due to price index fluctuations arising from the differing attributes of units sold in Q3 vis-a-vis Q4 last year.”

More News

GuocoLand taps X factor to help tenants pull workers to offices amid hybrid work

It finds that Grade A office buildings need to have a range of amenities, be in a vibrant location for greater appeal to occupiers seeking to build social capital Read MoreSingapore offices await a new wave of tenants

Landlords don’t know who the next occupants will be as the tech industry cycle which has provided demand for working spaces comes to an end Read MoreSingapore office rents in central region fall 1.7 per cent in Q1 after rising for 9 quarters

Tech, flexible space and traditional banking sectors adopt more conservative stance, mitigating rent-increase pressures Read MoreDBS puts 46 retail units, HDB shops on market for S$210 million

The units, previously occupied by full-service bank branches, are in places such as Bishan, Jurong West and Thomson Plaza Read MoreCiti Commercial Pte Ltd is founded in 2009. Since then, we have created a strong market presence in the commercial real estate consultancy with our dedication and consistent good service.

© Copyright 2024 Citi Commercial Pte Ltd :: Agency Licence No. L3009610D