- News

- Office investment sales headed for slow start in 2023 amid price gap, higher borrowing costs

Office investment sales headed for slow start in 2023 amid price gap, higher borrowing costs

THE market for big-ticket sales of office assets is heading for a slow start in 2023 – after a weak performance in the last two quarters of this year.

A significant buyer-seller price gap will continue to be a major hurdle in sealing deals – especially for income-generating office assets.

“Institutional buyers will probably watch and wait for a few more months, for visibility on interest rates peaking before jumping in,” said Jeremy Lake, managing director of investment sales and capital markets at Savills Singapore.

The surge in borrowing costs this year has eroded investors’ returns significantly. “In addition, in some cases, asking prices probably overshot the market and this has deterred buyers,” said Lake.

Wong Xian Yang, Cushman & Wakefield’s head of Singapore research, said that given higher financing costs and still-low yields for stabilised office assets, investors hunting for higher returns may have to look for value-add opportunities, that is, buildings with potential for asset enhancement or redevelopment.

They could also extend their search to non-core Central Business District (CBD) office submarkets (such as Bugis, City Hall and Orchard) and decentralised office markets (such as Jurong, Paya Lebar, Tampines and the Harbourfront/Alexandra locales), where there is potential for rents to be readjusted higher.

Wong also expects family offices and ultra-high-net-worth individuals (UHNWIs) to continue making more bite-sized investments such as strata offices and smaller office buildings in the CBD. “Many of these investors have deep cash reserves and are able to finance the deal in full cash or take up smaller loans; they are investing for wealth preservation or diversification.”

"The resilience of the office market will provide the platform for investors to reignite their interest to acquire office assets – when interest rates stabilise at levels that can provide positive carry in their acquisitions.” MICHAEL TAY, CBRE

Savills’ Lake, too, expects to see more investors from China, along with a trickle of UHNW European buyers, keen on strata offices and smaller office blocks – as well as shophouses and boutique hotels – in Singapore.

In contrast, purchases of larger office buildings by institutional investors will remain thin in the near term as borrowing costs have outstripped office yields, said observers.

Nagative carry

Lake said: “In January, investors could borrow at 1.5 per cent all in and office net yields were around 3 per cent, so it was all good. Today, borrowing costs range from 4.5 per cent to 5 per cent, all in. So, 3 per cent office yields don’t work.”

Observers said that a lack of distress sales and a buyer-seller price mismatch also point to a dearth of big office deals over the next few months at least.

Explaining the stalemate between potential buyers and sellers, Cushman’s Wong said: “On the one hand, CBD Grade A office rents have been on an uptrend and, coupled with low vacancy rates, sellers are not incentivised to lower their asking prices. On the other hand, borrowing costs rising rapidly to levels above office yields have pulled institutional investors such as core investment funds to the sidelines, as they await greater clarity and more attractive pricing.”

According to market watchers, there is a list of office buildings on the island that were put on the market – whether officially or privately – that are yet to be sold. These include Robinson 77, 78 Shenton Way, Bugis Junction Towers, Parkview Square, and 7 and 9 Tampines Grande.

According to Savills Research’s compilation of office transactions of at least S$10 million each up to Dec 21, the year-to-date tally stands at slightly over S$7.04 billion.

The figure is ahead of the S$5.16 billion for the whole of 2021.

Investors started 2022 with a positive outlook for the Singapore office market. “The fundamentals looked compelling and 10/10 investors were looking favourably at the sector,” said Lake.

CBRE’s head of research for South-east Asia, Tricia Song, said that return-to-office arrangements contributed to a more optimistic outlook towards future office leasing demand.

“Q1 2022 saw several big-ticket office transactions as... funds positioned themselves to capitalise from anticipated steady rental growth, limited new supply, strong leasing demand from technology companies and Singapore’s incipient economic recovery.”

Savills figures show the Q1 2022 office investment sales figure at S$4.7 billion – a big increase from the amount of about S$1.9 billion in Q4 2021, and S$992.6 million in Q1 2021.

Major deals in Q1 2022 included CapitaSky at 79 Robinson Road (S$1.26 billion), Cross Street Exchange (S$810.8 million) and Twenty Anson (S$598 million).

“The positive buying sentiment carried over into the second quarter after the full reopening of Singapore’s borders in April 2022,” said Song.

Singtel-Lendlease deal

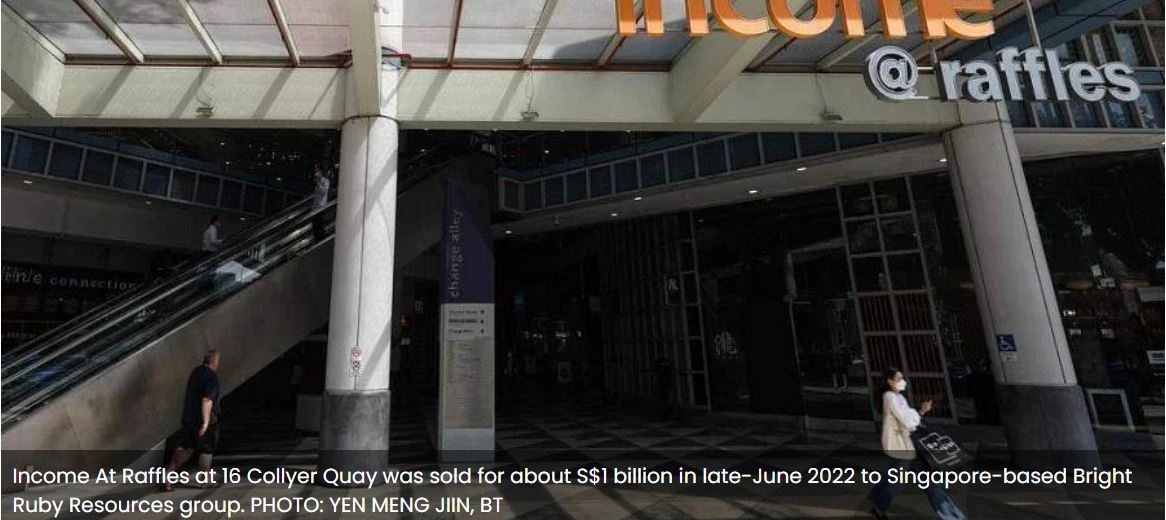

According to Savills, some S$1.9 billion of office assets were sold in Q2 2022; these include Income At Raffles at 16 Collyer Quay (the former Hitachi Tower) at about S$1 billion and Westgate Tower in Jurong East for S$680 million.

Savills did not include in its second quarter numbers Singtel’ : Z74 -0.4%s S$1.63 billion sale (announced on Jun 1) of its headquarters along Exeter Road to a joint venture (JV) with Lendlease, for the site’s redevelopment into a predominantly office project. The JV company will make the payment to Singtel in or around 2024, and Savills will reflect the transaction in its investment sales figures when that takes place.

If the property consulting group had counted this transaction under Q2 2022, its total office investment sales number for the quarter would have been a sizeable S$3.5 billion, though lower than the Q1 2022 figure.

When asked at what point did office sales begin to slow down, Lake said: “Cracks had started to appear at the end of Q1 as investors became more and more concerned about the headwinds arising from inflation, the war in Ukraine, the sharp stock market correction in the US, higher interest rates, China’s economic slowdown, and talk of recession.”

Office investment sales tanked to S$251 million in the third quarter. The Q4-to-date number, as at Dec 21, was at nearly S$200 million. “The speed and size of the increase in interest rates caught everyone by surprise,” said Lake.

Giving her take on big-ticket office deals in 2023, JLL Singapore’s head of research and consultancy Tay Huey Ying said: “We expect investors to be increasingly selective and cautious, resulting in the conclusion of deals for only very prime and strategic assets as well as those with reasonable asking prices.”

Said Wong of Cushman: “We are cautiously optimistic that office investment sales volume could recover in the later part of 2023 with potentially more clarity on interest rate trajectory, with the pace of US interest rate hikes expected to slow in the year. This would aid price discovery and facilitate deals.”

Savills’ Lake’s advice to potential buyers is: “Buy the dip. The office fundamentals remain compelling with an expected shortage of CBD office space in the next few years. Also, interest rates will normalise in the next 12 to 24 months, so high interest rates are an aberration.”

Making a similar case, CBRE’s head of capital markets for Singapore Michael Tay said that the impact of the tech sector’s slowdown on leasing demand for Singapore office space may, to some extent, be offset by other demand drivers as well as tenants displaced from older buildings to be pulled down for redevelopment, looking for replacement offices.

“Any downward pressure on rent from potential shadow space may also be less profound in an environment where new office supply will remain tight through the next three to four years,” said Tay, who was a veteran office leasing agent at CBRE before he moved to the capital markets team three years ago.

Phase of moderate office rent growth

He added that the above factors should support continued growth of Singapore office rents, although the market may go through a phase of moderate rental growth compared with projections of 12 months ago.

“Thus, the resilience of the office market and the likelihood of continued rental growth will provide the platform for investors to reignite their interest to acquire office assets when interest rates stabilise, at levels that can provide investors with confidence of positive carry – property yield exceeding borrowing cost – in their acquisitions,” Tay added.

Lake’s advice to potential sellers of Singapore office assets is to “either KIV selling until 2024 and beyond, or accept that the price has dropped by not less than 10 per cent”.

More News

Shopee’s parent Sea seen consolidating Singapore footprint in one-north, Science Park

The NYSE-listed group is no longer looking for a replacement tenant for 200,000 sq ft of office space it leased in Rochester Commons Read MoreJack Ma’s wife said to have bought three adjoining shophouses on Duxton Road

Zhang Ying, a Singapore citizen, paid about S$45 million to S$50 million for 70, 71 and 72 Duxton Road Read MoreMeta giving up 7 office floors totalling 115,000 sq ft at South Beach Tower

Landlord South Beach Consortium was informed in June 2023 and is in advanced negotiation with a replacement tenant for two whole floors Read MoreStrata office deals inch up 1.8% to S$1.2 billion, average price climbs 15% in 2023: Knight Frank

Knight Frank expects the strata office market to run up a total transaction value of S$1 billion in 2024 Read MoreCiti Commercial Pte Ltd is founded in 2009. Since then, we have created a strong market presence in the commercial real estate consultancy with our dedication and consistent good service.

© Copyright 2024 Citi Commercial Pte Ltd :: Agency Licence No. L3009610D